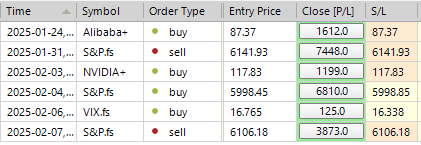

SP500 LDN TRADING UPDATE 10/02/25

SP500 LDN TRADING UPDATE 10/02/25

WEEKLY BULL BEAR ZONE 6114/24

WEEKLY RANGE RES 6114 SUP 5918

DAILY BULL BEAR ZONE 6010/00

DAILY RANGE RES 6091 SUP 6008

WEEKLY ACTION AREAS & PRICE OBJECTIVE VIDEO TO FOLLOW AHEAD OF THE NY OPEN

GOLDMAN SACHS TRADING DESK VIEWS

markets / macro: no straightforward days. FICC and Equities

The trading environment in recent weeks has been extremely intriguing, with no straightforward days, as the markets bounce from one headline to another. Specifically regarding US equities, the reality is this: we've been trading these same levels in the S&P repeatedly over the past three months; as a colleague remarked, “we’re running hard to stand still.” Despite this heightened difficulty, it could certainly be worse; the S&P is just 1.5% away from its highs, and market breadth is excellent. The takeaway thus far is that markets resemble jigsaw puzzles, and the current assembly is more challenging than before. To be honest, we've been spoilt in recent years; at this time last year, the S&P had experienced upward surges in 14 out of 15 weeks. Looking ahead, while I firmly believe we are still in a bull market, one should reasonably anticipate less consistency AND convexity than what we've become accustomed to. Concerning the opportunity landscape in macro trading, I think the main focus will be on preserving capital as early policy decisions unfold and being ready to pounce on 3-4 significant trends that will inevitably emerge.

GS US TMT: .. what a week ..

This has been one of the least gratifying weekly moves of about 6 bps that I’ve observed in some time, as the incorrect earnings price reactions were exacerbated by the increasingly shifting thematic landscape (Tariff complexities + DeepSeek effects).

Although the overall takeaways for TMT remain ‘solid’—the NDX is still hovering around ATHs (and above its 50-dma) & desk flows were more inclined towards buying last week (refer to GS PB’s latest)—IT Spending metrics continue to show strength (CTSH, NET), AI capital expenditures are unexpectedly strong in CY25 (AMZN, GOOG), there are signs of short-cycle industrial recovery (ISM data), ad expenditure is stable (PINS, GOOG, META), and the US Consumer is still relatively robust (EXPE, AFRM)—it has been challenging to identify a singular theme or trend to focus on so far in 2025 as cyclicals remain stagnant (Semis/SOX flat YTD), AI stocks experience volatility (cue DeepSeek), Large Cap software struggles (CRM, WDAY, INTU, MSFT types), and big Tech didn’t fare well in the 4Q earnings reports (only META is performing well YTD). In other words, high valuations and expectations are encountering increasing unease in price movements as we enter the third year of this AI capital cycle—the chart below shows the lack of “reward” for companies during the EPS season thus far.

... Looking forward, while numerous TMT companies have managed to move past the 1Q/CY25 guidance obstacles that dampened sentiment during preview season (consider NET, PINS, SPOT, TTWO ‘clearing event’ reactions)—it seems that investors are beginning to embrace a hint of optimism regarding 2Q/2H+ inflections across TMT—e.g., 1Q may be perceived as the “low point” for year-over-year growth in many areas of TMT as you overcome 1x headwinds (leap day, FX), encounter softer comps, and/or leverage idiosyncratic drivers (Blackwell ramp, Public Cloud capacity, Autos/Industrials bottoming, PC/Phone cycles, ‘recovery’ in Fed spending, etc)—which we will need to keep an eye on as we proceed into conference season over the coming weeks.

Russell 2k Futures: Unhealthy

The positioning of Russell 2k Non-Dealer futures has seen a continued decline heading into 2025, particularly around the end of January. This drop has been driven by the liquidation activities of Asset Managers. Key factors that likely contributed to this trend include a decline in cyclical momentum and the advancement of RFK Jr. for the position of health secretary by the Senate Finance Committee. In the following sessions, Russell 2k faced challenges alongside a decrease in the pricing of projected 2025 rate cuts, persistent health concerns, and diminishing optimism among small businesses. Nevertheless, Russell 2k's three-month funding improved and outperformed the S&P 500, leaving us curious about whether Russell 2k futures flows will stabilize.

The Non-Dealer positioning of Russell 2k futures continued its downward trend into 2025 as we approached the end of January. According to the Commitment of Traders report, Non-Dealers sold $830 million between January 28 and February 4, marking a fifth consecutive week of bearish activity totaling $9.3 billion. Consequently, Non-Dealer net length has dropped to its lowest level since early September.

Asset Manager liquidation has been the most significant factor here. In the latest data, Asset Managers accounted for the largest sales at -$2.2 billion, primarily due to unwinding of long positions worth -$1.6 trillion. This trend has significantly impacted the broader Non-Dealer shift. Specifically, from December 31 to February 4, Asset Managers sold -$6.2 billion with long positions decreasing by -$5.2 billion.

Contributing factors have included a reduction in cyclical momentum along with the Senate Finance Committee's advancing of RFK Jr. for health secretary. From January 28 to February 4, GS's US Cyclicals index experienced a drop of -1.7%. Additionally, GSXUMAHA, a gauge of US listed firms at risk from potential health regulations under the new administration, fell by -1.2%. Asset Manager long positions are positively correlated with both of these indices, though it's arguable that Asset Managers may have anticipated or overshot the changes in Cyclicals.

In subsequent trading sessions, Russell 2k continued to struggle in the context of decreasing expectations for rate cuts in 2025, ongoing health issues, and declining small business sentiment. Between February 4 and 7, Russell 2k decreased by -0.5%. Data on the US labor market showed upward revisions to previous months and exceeded consensus on average hourly earnings, resulting in a 9 basis point drop in December 2025 SOFR. GSXUMAHA lost an additional -1%, and GS's Small and Medium-Sized Business index declined by -0.4%.

However, it is worth noting that Russell 2k's three-month funding improved, allowing it to outperform the S&P 500. It will be intriguing to see if the flows in Russell 2k futures find stability.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!