Institutional Insights: Goldman Sachs AUDNZD

AUD/NZD: Deserved Divergence, but Positioning Is Getting Stretched

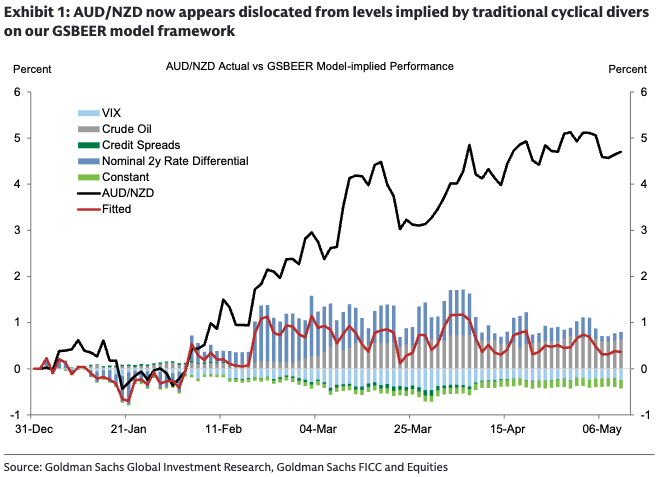

AUD has been one of the strongest G10 currencies since the start of the energy shock, and AUD/NZD is now at its highest level in more than a decade. The move looks extended versus traditional cyclical models, but it is not irrational. The key point is that relative terms of trade have become the dominant FX driver, and that has favored Australia over New Zealand.

Australia benefits from commodity exposure, especially metals and energy-linked terms-of-trade effects. New Zealand, by contrast, is more exposed as an energy importer. So even though AUD/NZD screens rich versus traditional drivers like rate differentials, credit spreads, VIX, and crude in the GSBEER framework, the outperformance looks broadly justified by the current macro regime.

Main message

AUD/NZD looks stretched, but not yet fundamentally wrong. The rally is supported by terms-of-trade divergence, higher oil, Australia’s commodity beta, and a relatively hawkish RBA. However, positioning is now crowded enough that the cross is vulnerable to a reversal if the RBA turns less hawkish, Australian domestic data weaken, or energy prices fall on sustained Middle East de-escalation.

In short: deserved divergence for now, but no longer a clean chase.

Why AUD has outperformed

AUD outperformance did not start with the energy shock. AUD was already the strongest G10 currency in January and February, supported by its beta to metals prices and improving relative terms of trade. Since the energy shock began, that support has broadened because higher energy prices have favored Australia relative to New Zealand.

The traditional cyclical model says AUD/NZD is now roughly 4 percentage points above where it “should” be based on usual drivers. But those models are capturing less of FX price action than usual because FX markets have shifted away from rate differentials and toward commodity/terms-of-trade dynamics.

That matters because AUD/NZD is not simply trading on RBA versus RBNZ policy. It is trading as a relative commodity importer/exporter expression.

Terms of trade: the core driver

The most important distinction is Australia’s commodity leverage versus New Zealand’s energy-importer exposure.

Australia benefits from:

Metals exposure

Commodity-linked income support

Improved export pricing

Positive sensitivity to higher global commodity prices

Better relative terms of trade versus the US and New Zealand

New Zealand is more vulnerable to:

Higher imported energy costs

Pressure on real incomes

Weaker external balances

Deteriorating relative terms of trade

Regional demand concerns

This is why AUD/NZD has rallied even though traditional cyclical drivers look less supportive. The terms-of-trade channel explains why the move has persisted.

Oil days reveal the market’s bias

One of the clearest signals is AUD/NZD’s asymmetric performance on oil-up days. Since the conflict began, most trading days have fallen into three regimes:

Regime | AUD/NZD behavior |

|---|---|

Oil higher, US equities higher | AUD outperforms NZD |

Oil higher, US equities lower | AUD still tends to outperform NZD |

Oil lower, US equities higher | AUD/NZD gives back some gains |

The important part is the asymmetry. AUD/NZD has outperformed strongly when oil rises, but its retracement when oil falls has not been large enough to offset prior gains. That suggests investors believe the current environment remains supportive for AUD and that the terms-of-trade impulse is likely to persist.

But there is a warning: AUD/NZD underperforms on “de-escalatory” days when oil falls alongside risk assets. If markets start pricing a more durable end to the conflict and a shift from higher oil to lower oil, AUD/NZD could reverse.

Domestic backdrop: still supportive, but less clean

Australia’s domestic backdrop has also supported AUD. The RBA has been relatively hawkish and delivered a third consecutive 25bp hike at the May meeting, taking the policy rate back to 4.35%, the highest level in more than a decade.

That carry support matters. In a world where risk sentiment remains supported, AUD’s carry profile is increasingly attractive, particularly versus low-yielding or more vulnerable currencies.

But the domestic picture is no longer one-way bullish. Recent Australian data have become more mixed. Inflation was softer than consensus and below the RBA’s February SMP forecast, while survey data have deteriorated. Goldman economists still expect another RBA hike in June, but they also think domestic demand growth could undershoot the RBA’s forecasts through 4Q 2026, with financial conditions already materially tighter.

So the domestic policy support is real, but increasingly fragile.

Positioning: the main tactical risk

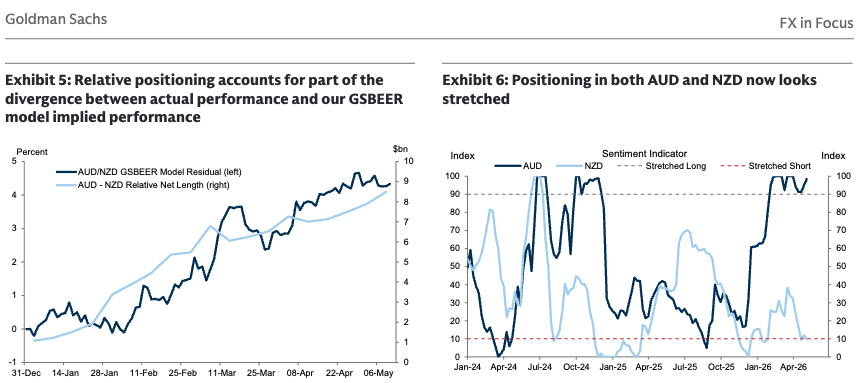

Positioning has likely helped drive the rally. Relative positioning has tracked closely with the move in AUD/NZD and seems to explain part of the divergence between actual performance and GSBEER-implied performance.

But positioning now looks stretched in both AUD and NZD. That raises the risk of an outsized move lower in AUD/NZD if the catalyst shifts.

The biggest reversal triggers are:

RBA communication turns less hawkish

Australian inflation or activity data disappoint

Energy prices fall meaningfully

Middle East de-escalation becomes durable

Commodity prices soften

Risk sentiment deteriorates

Crowded AUD longs are forced to reduce

This does not mean AUD/NZD must reverse immediately. It means the risk/reward has shifted from clean long to selective long / buy dips / avoid chasing breakouts.

AUD versus USD still looks better than AUD versus NZD

Even if AUD/NZD reverses, AUD could still remain a relative outperformer, especially versus USD, if risk sentiment stays supported and Australia’s carry proposition remains constructive.

That distinction is important. AUD/NZD is now stretched because both the relative terms-of-trade and positioning stories are well recognized. But AUD/USD may still have upside if:

Global risk appetite remains firm

The Fed eventually cuts

The US dollar weakens

Metals stay supported

Australia’s carry remains attractive

China/regional demand stabilizes

So the better trade may shift from chasing AUD/NZD higher to expressing AUD strength more selectively, especially against the dollar on dips.

Trading implications

AUD/NZD: still fundamentally justified, but stretched. Higher-for-longer energy prices should continue to support the cross, but positioning makes it vulnerable to sharp pullbacks. Prefer buying dips rather than chasing highs.

AUD/USD: remains attractive if global risk sentiment is supported and Fed-cut expectations eventually weigh on the dollar. AUD can still outperform even if AUD/NZD consolidates.

NZD: remains vulnerable as long as high energy prices pressure terms of trade and regional demand. A sustained drop in oil or a stronger domestic data pulse would be needed to improve the setup.

Key monitor: AUD/NZD is one of the best FX barometers for how markets are pricing commodity prices, energy risk, and regional demand. If AUD/NZD keeps rising on oil-up days and barely falls on oil-down days, the market still believes the energy shock is AUD-supportive. If that asymmetry breaks, it would be an early signal of reversal risk.

Bottom line

AUD/NZD’s rally looks stretched versus traditional models, but it is not unjustified. The move reflects a genuine terms-of-trade divergence: Australia is benefiting from commodity exposure, while New Zealand is being hurt by higher imported energy costs.

For now, AUD/NZD deserves to trade rich as long as higher energy prices remain central to the macro backdrop. But positioning is increasingly crowded, and domestic support from the RBA may be less reliable if data soften. The cross remains a useful long while the energy shock persists, but the tactical risk/reward now favors holding or buying dips, not aggressively chasing new highs.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!